- HR:+91-879-9184-787

- Sales:+91-908-163-7774

U.S. businesses face mounting financial complexity, driven by remote operations, tighter compliance rules, and an increasingly global workforce. AI in Accounting and Auditing practices often leads to human error, limited visibility, and slow reporting cycles.

This is where AI in accounting and auditing steps in, not as a replacement for finance professionals, but as an intelligent extension of them. From streamlining invoice processing to flagging anomalies in real-time, AI is transforming financial governance at every level.

In this blog, we’ll explore what this transformation means for startups and enterprises, the ROI potential, implementation strategies, and why it’s essential to work with the right AI development partner.

AI in accounting and auditing refers to the integration of artificial intelligence technologies such as machine learning, natural language processing, and intelligent automation into financial workflows to improve accuracy, efficiency, and compliance. Rather than replacing accountants or auditors, AI enhances their capabilities by handling repetitive tasks, uncovering insights in large volumes of data, and ensuring continuous financial oversight.

In accounting, AI automates processes such as:

In auditing, AI shifts the traditional model from sample-based, periodic reviews to real-time, full-population analysis. Tools can review thousands of transactions instantly, identify outliers, and generate detailed audit trails that enhance both internal and external audits.

By reducing human error, improving turnaround time, and enhancing visibility, AI in accounting and auditing is driving a shift toward continuous compliance and strategic financial governance, especially critical for U.S. enterprises navigating strict regulatory standards.

You may also want to know AI in Architecture

U.S. companies are increasingly adopting AI in finance to gain a strategic edge in a highly competitive, regulation-heavy, and fast-moving business environment. The shift is driven by three core needs: operational efficiency, compliance assurance, and data-driven decision-making.

Traditional finance departments often spend 60–80% of their time on manual, rules-based tasks like data entry, invoice matching, and financial reporting. AI automates these functions with higher speed and fewer errors, freeing up finance teams to focus on forecasting, scenario planning, and strategic initiatives. This is especially important for small and mid-sized U.S. businesses aiming to grow without inflating back-office costs.

With AI-powered analytics and predictive modeling, CFOs and finance leaders can move beyond static monthly reports to real-time dashboards that forecast revenue, detect liquidity risks, and model different growth scenarios. This agility is vital in volatile markets where quick, data-backed decisions impact survival and scalability.

U.S. companies operate under tight regulatory scrutiny, such as GAAP, SOX, and SEC reporting. AI tools help enforce compliance by monitoring every transaction for anomalies, generating audit trails automatically, and identifying risk exposures early. For public companies and those preparing for IPOs, this adds significant assurance.

As finance roles become more analytical and tech-driven, the talent pool is struggling to keep pace. AI fills the gap by handling repetitive, high-volume tasks and supporting lean finance teams with intelligent automation that scales as the business grows.

In short, U.S. businesses are turning to AI in finance not just to keep up, but to lead, optimizing cash flow, reducing risk, and enabling smarter, faster decision-making in a digital-first economy.

AI in accounting and auditing is not just a trend; it’s a transformative force that improves efficiency, accuracy, and compliance in financial operations. By automating repetitive tasks, providing real-time data insights, and enhancing decision-making, AI is reshaping how accounting and auditing functions are carried out. Below are the key use cases where AI is driving significant value for businesses:

One of the most time-consuming tasks in accounting is manually entering data from invoices, receipts, and other financial documents into accounting systems. AI-driven tools use Optical Character Recognition and Natural Language Processing to automatically extract and input relevant data into accounting software, significantly reducing human error and time spent on administrative tasks.

AI is particularly effective at identifying patterns that may indicate fraudulent activity or potential risks. Machine learning models are trained on historical transaction data to recognize unusual behaviors or discrepancies that may signal fraud or non-compliance. AI can monitor transactions in real-time, flagging anomalies such as unauthorized purchases or unusual financial activity.

AI helps finance teams move beyond static historical reports by enabling predictive analytics. Machine learning algorithms can analyze a company’s historical financial data, market trends, and external factors to provide accurate cash flow forecasts and help with financial planning.

Navigating the complex world of tax regulations is a challenge for businesses, especially in regions with changing tax laws. AI can automate tax calculations, ensure compliance with regulations, and even optimize tax strategies by analyzing large amounts of financial data to identify possible deductions and savings.

Traditional audits typically occur at fixed intervals, often quarterly or annually, but AI enables continuous auditing. With AI, auditors can analyze 100% of transactions in real-time, rather than relying on random sampling. This leads to more accurate audits, quicker identification of discrepancies, and more robust financial reporting.

Account reconciliation is a fundamental accounting process, but it can be tedious and prone to errors when done manually. AI tools can automatically match bank statements, invoices, and other financial records, highlighting discrepancies and suggesting corrections.

AI can streamline the process of generating financial reports by pulling data from various sources, automatically analyzing it, and generating insights into company performance. This can help finance teams create accurate and timely reports with far less effort than traditional methods.

Maintaining an audit trail is a critical part of ensuring compliance and transparency in financial practices. AI-powered systems can track and record every action in financial systems automatically, ensuring that audit trails are accurate, complete, and easily accessible for internal or external reviews.

The return on investment of AI in accounting and auditing is transformative, with AI tools offering significant benefits in terms of cost savings, efficiency, accuracy, and risk mitigation. By automating routine tasks, enhancing decision-making, and ensuring compliance, AI is helping companies not only streamline operations but also gain a competitive edge. Below, we’ll explore the tangible financial and operational benefits of AI adoption in accounting and auditing.

One of the most significant ways AI impacts ROI is by automating time-consuming tasks such as data entry, invoice processing, transaction categorization, and financial reconciliations. For example, instead of spending hours manually entering data from invoices and receipts, AI systems automatically extract and input the necessary information into accounting software.

AI enables near real-time financial reporting, drastically reducing the time it takes to close books at the end of each period. AI-powered tools can pull data from various sources, analyze it, and produce reports instantly.

Manual accounting and auditing processes are prone to human error, whether from fatigue, oversight, or simple mistakes. AI minimizes this risk by executing repetitive tasks with precision and consistency, reducing the likelihood of errors in financial reporting or audits.

Compliance is a critical issue for businesses, especially in industries like healthcare, finance, and manufacturing, where regulations such as SOX, GAAP, and the SEC guidelines must be adhered to strictly. AI can automate the monitoring of financial transactions and reporting to ensure compliance with these standards.

AI models trained on historical financial data can quickly detect outliers or fraudulent activity. These tools continuously monitor transactions and flag anything that deviates from normal patterns, such as unusually large payments, mismatched receipts, or duplicate entries.

AI can analyze large datasets to generate forecasts and predict future trends in cash flow, expenses, and revenue. By evaluating historical financial data, market conditions, and economic factors, AI provides more accurate projections, helping businesses make informed financial decisions.

As a company grows, its financial operations must scale accordingly. AI tools can handle increasing volumes of financial transactions, automate additional tasks, and provide real-time insights as the business expands, without the need for proportional increases in headcount.

AI’s ability to automate accounting and auditing tasks means firms can operate with fewer full-time employees, allowing businesses to reduce their reliance on high-cost accounting staff for routine tasks. This can result in substantial savings on salaries and overhead costs.

For accounting firms that offer audit services, AI accelerates the process by analyzing entire populations of transactions instead of random sampling. This leads to more accurate and timely audit reports, which are essential for client satisfaction.

Implementing AI in accounting and auditing is a significant investment, both in terms of time and money. However, the potential ROI from increased efficiency, reduced errors, and improved decision-making can more than justify these costs. Understanding the costs and timelines involved in integrating AI solutions into your financial operations is crucial for setting realistic expectations and planning a successful implementation. Below are the key cost and timeline considerations to keep in mind when adopting AI in accounting and auditing:

The initial costs of implementing AI in accounting and auditing include expenses for system integration, customization, software licenses, and the purchase of AI tools or platforms. These costs can vary widely depending on the complexity and scope of the project, as well as the type of AI technology being integrated.

AI systems require regular maintenance and updates to ensure that they continue to perform well, adapt to new challenges, and comply with evolving regulations. The ongoing costs for AI in accounting and auditing depend on the level of support and customization required.

For a successful implementation, your accounting and auditing teams must be trained to use AI tools effectively. Training costs depend on the complexity of the AI solutions and how many staff needs to be involved.

The timeline for implementing AI in accounting and auditing varies significantly based on the project scope, the tools you choose, and the size of your team. It’s important to understand that AI integration is not an overnight change; it’s a phased process that involves planning, development, testing, and training.

The ROI from AI in accounting and auditing can be substantial, but it requires time to materialize. While AI provides immediate operational improvements, such as automation and real-time reporting, its full financial benefits are realized over time through efficiency gains, error reduction, and improved decision-making.

As businesses grow, the volume of financial data and the complexity of accounting tasks increase. AI in accounting and auditing offers scalability, allowing businesses to automate more processes without the need for proportional increases in staff.

AI tools scale efficiently, enabling firms to handle increased transaction volumes, regulatory complexity, and diverse client needs without significantly adding to costs.

You may also want to know AI Brainstorming

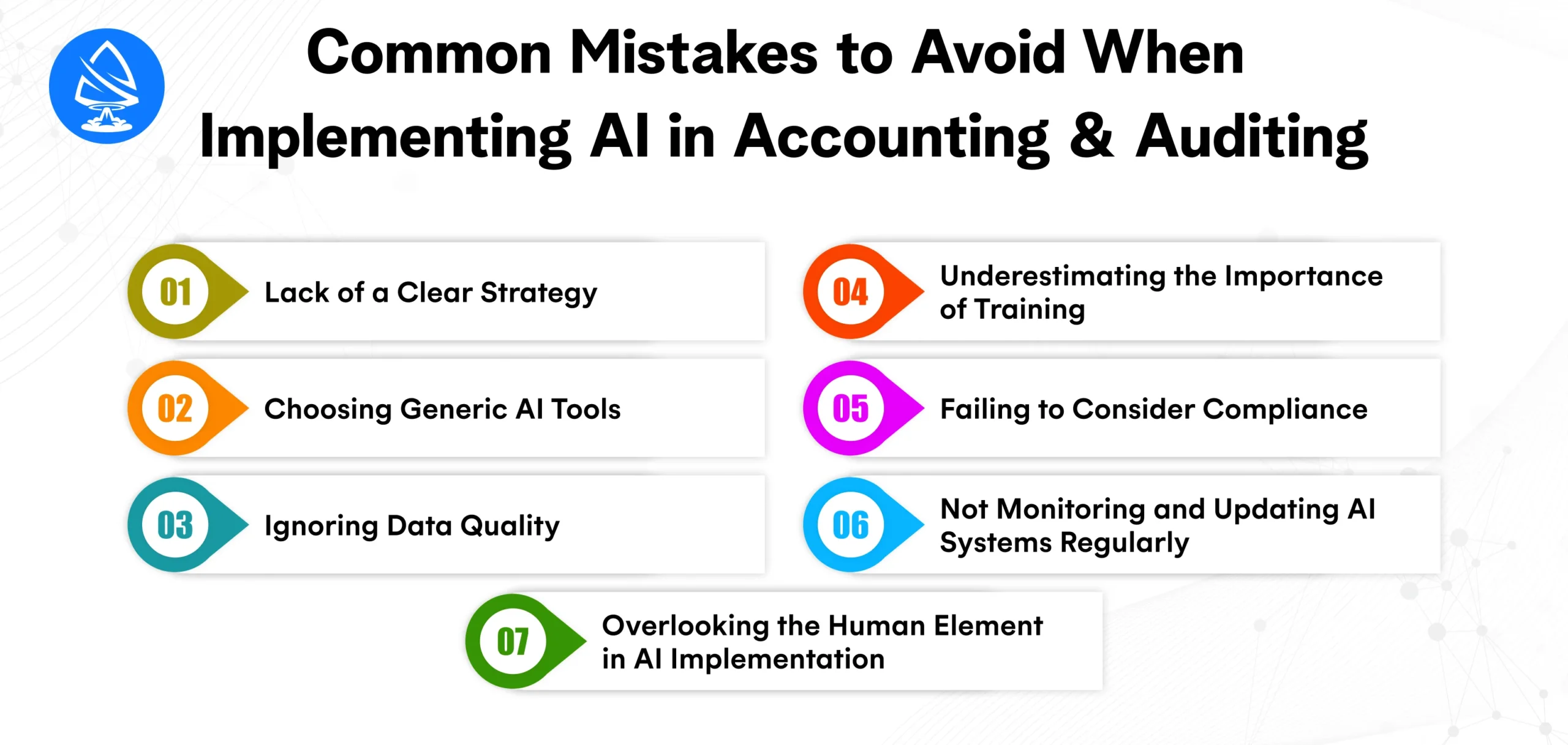

While AI has the potential to revolutionize accounting and auditing by improving accuracy, efficiency, and compliance, the implementation process can be complex. Many organizations make common mistakes during the adoption of AI in these areas, which can hinder the successful deployment of the technology and even lead to a negative ROI. By understanding and avoiding these common pitfalls, businesses can ensure that their investment in AI technology delivers the expected benefits.

A frequent mistake businesses make is rushing into AI adoption without first defining a clear use case. Implementing AI without identifying specific problems it will solve or areas where it can add value leads to underwhelming results and wasted resources.

Without a defined purpose, AI tools may end up being underutilized, resulting in a lack of clear ROI and business disruption. It’s essential to align AI adoption with strategic goals and high-value processes.

Many companies opt for off-the-shelf AI solutions that are not tailored to the specific needs of accounting and auditing. While these tools can be cheaper and faster to implement, they often lack the necessary customization and flexibility to address unique business requirements.

Generic tools may not integrate seamlessly with existing accounting software or might not offer the specific functionalities your team needs, resulting in inefficiencies and frustration.

AI systems rely heavily on the quality of the data they process. If the data used to train the AI models is incomplete, inaccurate, or inconsistent, it can lead to poor results. Additionally, integrating AI tools with legacy systems, such as outdated ERP software, can create barriers to successful implementation.

Poor data quality can result in inaccurate financial reports, missed fraud indicators, and suboptimal decision-making. Inadequate integration can create workflow bottlenecks, making the AI tools ineffective or redundant.

Another mistake is overlooking the need for comprehensive training and change management strategies. AI tools can be powerful, but they are often complex and require employees to adapt to new workflows. Without proper training, your team may resist the technology or fail to leverage it effectively.

Without adequate training, employees might struggle to use AI tools correctly, leading to inefficiencies and a lack of confidence in the technology. This can also result in lower adoption rates, hindering the full benefits of AI.

AI tools in accounting and auditing must be designed to meet various compliance standards, including those imposed by the Sarbanes-Oxley Act, Generally Accepted Accounting Principles, HIPAA for healthcare, and GDPR for data protection. Failing to consider these legal and regulatory requirements when selecting or implementing AI systems can lead to costly penalties or compliance issues.

Non-compliance can result in legal risks, financial penalties, and reputational damage, especially if AI is used in ways that violate privacy laws or other regulatory requirements.

AI systems require ongoing monitoring and maintenance to remain effective. Failure to periodically update models, track performance, and retrain algorithms based on new data can result in models that are outdated, inaccurate, or inefficient.

Unmonitored AI tools may perform poorly over time, leading to inaccurate financial data, missed fraud, or unoptimized processes. This diminishes the overall value of the investment and can hurt business operations.

AI is often seen as a tool that can completely replace human involvement in financial tasks. However, the best results come when AI supports, rather than replaces, human expertise. Over-relying on AI or neglecting the input of skilled accountants and auditors can result in overlooked nuances and missed opportunities.

AI can automate many tasks, but it still requires human oversight to ensure that complex, context-sensitive decisions are made. Without human judgment, AI can produce outputs that may not align with business goals or customer expectations.

Artoon Solutions specializes in AI development for regulated industries, with a proven track record supporting U.S. clients in fintech, accounting, and ERP automation.

Why leaders choose Artoon:

As U.S. financial operations become more data-driven, AI is no longer optional; it’s a growth enabler. For CFOs, controllers, and finance teams, investing in AI for accounting and auditing is the clearest path to transparency, speed, and risk reduction.

Whether you’re modernizing a legacy finance stack or building a digital-first back office from scratch, Artoon Solutions can help.

Book a Free Consultation or use our AI Cost Calculator to estimate your project budget today.

1. What are the top AI tools used in accounting?

QuickBooks AI, Xero with AI add-ons, MindBridge AI Auditor, and custom ML models for ERP systems.

2. Can AI replace accountants?

No. AI augments finance teams by automating repetitive tasks, while accountants still handle judgment-based work.

3. Is AI auditing compliant with regulations like SOX?

Yes, if implemented with proper controls and audit logs.

4. How long does it take to implement an AI auditing system?

4 to 12 weeks, depending on scope and integration requirements.

5. What’s the ROI of AI in auditing?

Most U.S. businesses see a 30–50% efficiency gain and faster compliance.

6. What’s the cost of custom AI accounting solutions?

Starting from $15,000 for basic automation, scaling up based on features.

7. Do I need internal IT support to use AI in accounting?

Not necessarily. Artoon Solutions offers end-to-end managed services.

8. How secure is AI for financial data?

AI systems are built with encryption, role-based access, and SOC 2-compliant architectures.

Artoon Solutions

Artoon Solutions is a technology company that specializes in providing a wide range of IT services, including web and mobile app development, game development, and web application development. They offer custom software solutions to clients across various industries and are known for their expertise in technologies such as React.js, Angular, Node.js, and others. The company focuses on delivering high-quality, innovative solutions tailored to meet the specific needs of their clients.